Author

Annual Investment Allowance

Published 28 September 2021

The Finance Act 2021

‘In its ordinary sense it (that is, plant) includes whatever apparatus is used by a businessman for carrying on his business – not his stock-in-trade which he buys or makes for sale; but all goods and chattels, fixed or movable, live or dead, which he keeps for permanent employment in the business.’

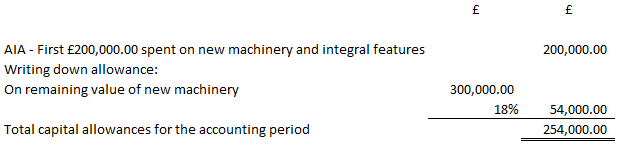

What this means for your business

What we can do for you

[1] S.32 Finance Act 2019.

[2] S.15 Finance Act 2021.

[3] Practical Law, Capital Allowance. Available at: https://uk.practicallaw.thomsonreuters.com/4-107-5846?transitionType=Default&contextData=(sc.Default)&firstPage=true [Accessed August 30, 2021].

[4] SS.51A to 51N Capital Allowance Act 2001.

[5] Cambridge Dictionary, Capital Asset. Available at: https://dictionary.cambridge.org/dictionary/english/capital-asset [Accessed August 30, 2021].

[6] (1887) 19 QBD 647.

[7] What You Can Claim On. Available at: https://www.gov.uk/capital-allowances/what-you-can-claim-on [Accessed August 30, 2021].

[8] Annual Investment Allowances. Available at: https://www.gov.uk/capital-allowances/annual-investment-allowance [Accessed August 30, 2021].